Understanding the Withdrawal and Re-Contribution Strategy

- Luke Palmer

- Dec 1, 2025

- 2 min read

Following our recent article HERE on how superannuation benefits are taxed when passed to beneficiaries, one strategy worth exploring in more detail is the withdrawal and re-contribution strategy. This approach can be a powerful tool for improving estate planning outcomes and reducing tax for non-tax dependent beneficiaries.

What Is a Withdrawal and Re-Contribution Strategy?

A withdrawal and re-contribution strategy involves:

Withdrawing a portion (or all) of your superannuation balance.

Re-contributing the withdrawn amount back into your superannuation account as a non-concessional (after-tax) contribution.

The goal is to convert taxable components of your super into tax-free components, which can significantly reduce the tax payable by your beneficiaries upon your death.

Why Consider This Strategy?

This strategy may be beneficial for:

Estate planning: Reducing the taxable portion of your superannuation can lower the tax burden for adult children or other non-tax dependent beneficiaries.

Maximising tax-free benefits: Increasing the tax-free component of your super can help ensure more of your wealth is passed on without erosion from tax.

Simplifying distributions: A cleaner superannuation structure may make it easier for your executor or legal personal representative to manage your estate.

Who Might Benefit Most?

This strategy is typically suited to:

Retirees or those nearing retirement, especially individuals aged 60 or over who can access their super tax-free.

Individuals with large taxable components in their superannuation balance.

Those with adult children or other non-tax dependent beneficiaries who would otherwise face tax on inherited super.

Key Considerations and Risks

Before implementing this strategy, consider the following:

Timing and liquidity: You must have access to your super and the ability to re-contribute within the allowable timeframes.

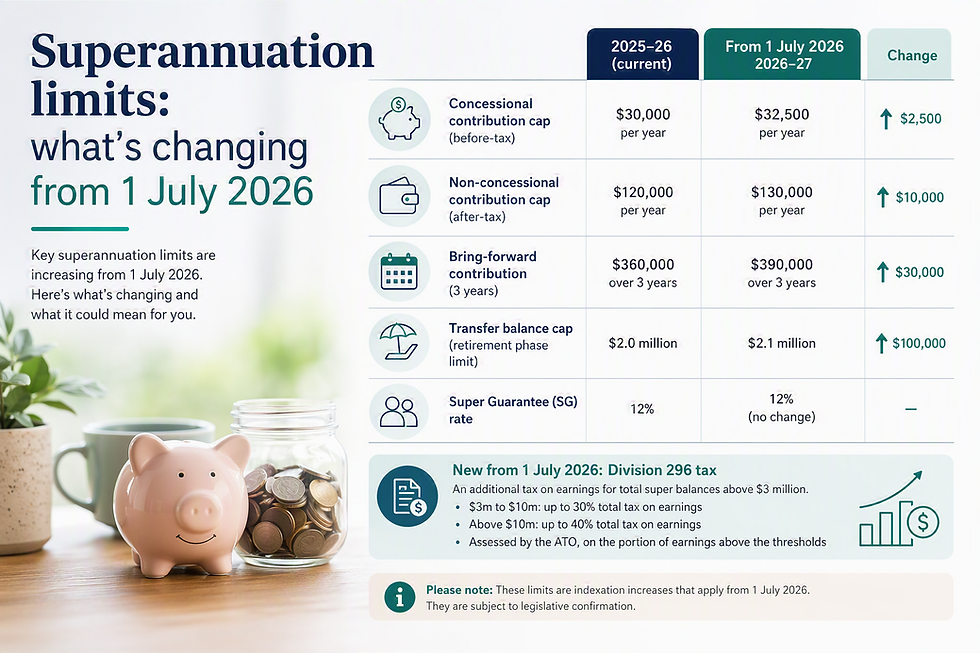

Contribution caps: Non-concessional contributions are subject to annual limits. Exceeding these can result in penalties.

Age restrictions: Individuals over 75 may face limitations on making contributions.

Centrelink implications: Re-contributing funds may affect your eligibility for government benefits.

Estate planning alignment: Ensure this strategy fits within your broader estate planning goals and legal arrangements.

Example Scenario

Let’s say you have a superannuation balance of $600,000, with $400,000 in taxable components and $200,000 in tax-free components. By withdrawing $300,000 and re-contributing it as a non-concessional contribution, you could shift a significant portion of your balance into the tax-free category—potentially saving your adult children thousands in tax.

Next Steps

If you're considering a withdrawal and re-contribution strategy:

Speak with a financial adviser to assess your eligibility and suitability.

Review your contribution limits.

Consider the timing and structure of your estate plan.

If you have questions about whether this strategy is right for you, or how it could impact your beneficiaries, feel free to reach out for a personalised discussion.

Comments