The 2026-27 Federal Budget: What It Means for You

- Luke Palmer

- May 13

- 5 min read

The Australian Government handed down its Federal Budget on 12 May 2026, announcing a wide-ranging package of tax, superannuation, health and aged care measures. Whether you are working, approaching retirement, or already enjoying it, there is likely something in this Budget that touches your financial life. Here is a clear summary of the key announcements.

Tax Cuts Already on the Way

Tax cuts that have already been legislated will see the lowest marginal tax rate — the rate that applies to taxable income between $18,201 and $45,000 — reduced from 16% to 15% from 1 July 2026, and then further to 14% from 1 July 2027. Every Australian taxpayer earning above the tax-free threshold stands to benefit, with savings of up to $268 in 2026–27 and up to $536 in 2027–28 compared with current settings.

For seniors, these cuts also raise the effective tax-free thresholds. For example, by 2027–28, a single person eligible for both the Low Income Tax Offset (LITO) and the Seniors and Pensioners Tax Offset (SAPTO) would have an effective tax-free threshold of $38,147 — meaning you could earn up to that amount from certain income sources before paying income tax.

A Simpler Way to Claim Work Expenses

From the 2026–27 income year, a new $1,000 instant tax deduction for work-related expenses will be available. If your total work-related expenses are under $1,000, you can simply claim the deduction without needing to keep receipts or itemise individual costs. You can also still claim deductions for income protection insurance premiums and union or professional association membership fees on top of this amount.

If your work-related expenses exceed $1,000, you can choose not to use the instant deduction and instead claim under the existing rules in the usual way — though you will need to keep appropriate records.

A New Tax Offset for Workers

From the 2027–28 income year, the Government will introduce the Working Australians Tax Offset (WATO) — a permanent $250 tax offset applied automatically when you lodge your tax return. It applies to income earned from work, such as wages and salaries or sole trader business income, and operates in a similar way to the existing Low Income Tax Offset.

The WATO will increase the effective tax-free threshold for workers by nearly $1,800. For those eligible for both LITO and SAPTO, the effective tax-free threshold rises to $38,940 for a single person and $34,726 for each member of a couple.

Changes to Capital Gains Tax

One of the most significant announcements is the reform of capital gains tax (CGT). From 1 July 2027, the familiar 50% CGT discount will be replaced by a cost base indexation method — calculated using the Consumer Price Index — for assets held longer than 12 months. In addition, a minimum 30% tax rate will apply to net capital gains. These changes apply to all CGT assets, including property and shares, held by individuals, trusts and partnerships. Pre-1985 assets are also affected.

Transitional rules will protect existing holdings. Assets bought and sold before 1 July 2027 remain entirely under the current rules. For assets owned before 1 July 2027 and sold afterwards, gains accrued up to that date will still receive the 50% CGT discount, while gains accrued from 1 July 2027 will be calculated under the new indexation method. You will need to determine the value of your asset as at 1 July 2027 — either through a formal valuation or by using an apportionment formula the ATO will provide.

Importantly, investors in new-build residential properties will retain the choice of the 50% CGT discount or the new indexation method. Income support recipients, including Age Pension recipients, will be exempt from the minimum tax. Superannuation funds are not affected and will continue to receive a one-third CGT discount.

Negative Gearing Reforms

From 1 July 2027, negative gearing on established residential properties will be restricted. Losses from these properties will only be deductible against rental income or capital gains from residential property. Any excess losses can be carried forward to offset residential property income in future years.

Transitional rules apply here too. Properties you already hold at the date of announcement — including those under contract but not yet settled — are exempt. Properties purchased between the announcement and 30 June 2027 may be negatively geared during that window, but not from 1 July 2027 onwards. New-build properties, properties held in superannuation funds (including SMSFs), and those in widely held trusts remain eligible for negative gearing.

Minimum Tax on Discretionary Trusts

From 1 July 2028, a 30% minimum tax will apply to the taxable income of discretionary trusts, paid by the trustee. Beneficiaries (other than companies) will receive a non-refundable tax credit for the tax paid. Several trust types are exempt, including fixed trusts, superannuation funds, special disability trusts, deceased estates, charitable trusts and discretionary testamentary trusts that existed at announcement. To support small businesses that wish to restructure, expanded rollover relief will be available for three years from 1 July 2027.

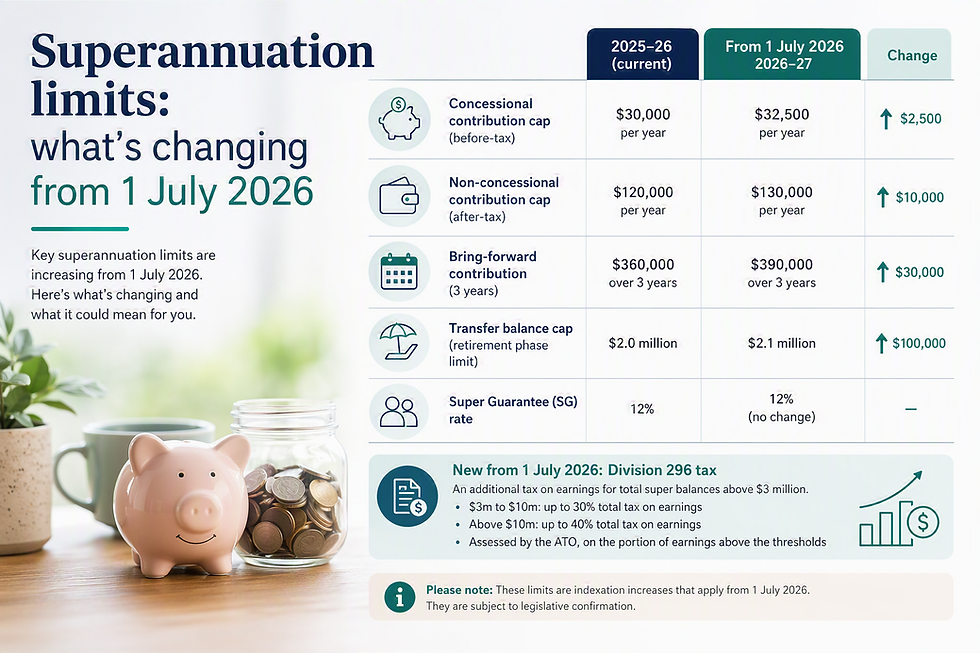

Superannuation

Payday Super commences 1 July 2026, requiring employers to pay Super Guarantee contributions at the same time as wages rather than quarterly — making it easier for you to track whether your super is being paid on time.

The new Division 296 tax also takes effect from 1 July 2026. It applies an additional 15% tax on superannuation earnings attributable to total balances above $3 million, and a further 10% (25% total) on earnings above $10 million. The tax is assessed to the individual, who may choose to pay it personally or have it released from their super fund.

Private Health Insurance

From 1 April 2027, the age-based uplift on the private health insurance rebate will be removed. Currently, policyholders aged 65 and over receive a higher rebate percentage than younger Australians at the same income level. Under the proposed change, a single flat rebate rate will apply regardless of age.

Aged Care

From 1 July 2026, the Government will fund an additional 5,000 aged care beds each year, primarily for those with limited financial means. Access to home care will also be improved, with personal care services — such as showering, dressing and incontinence aids — to be fully funded under the Support at Home program. Additional investment in dementia care and workforce supports is also included.

Electric Vehicles

The fringe benefits tax (FBT) exemption for eligible electric cars valued up to $75,000 will continue for arrangements entered into before 1 April 2029. From that date, a permanent 25% FBT discount will apply for electric cars valued up to the fuel-efficient luxury car tax threshold (currently $91,387).

If you would like to discuss how the budget announcements may impact you, please don't hesitate to contact us.

This article is general information only and does not constitute personal financial advice. It is based on the Federal Budget announcements of 12 May 2026 and proposed measures are subject to the passage of legislation.

Comments